In my previous post I discussed the struggle with staying in an

optimistic entrepreneurial mindset when you feel like all of the good

ideas are gone, the market is saturated, and opportunity has left the

building. I surmised that this is just a feeling and not reality. Well,

along the same lines, I have another question I want to ask you about.

A few weeks back Seth Godin wrote a post about Same as it ever was

where he displayed two of the first portraits ever taken and basically

as asked: could they have been taken with Instagram? The point he was

making (in my opinion) is that there's plenty of opportunity in

products, services or technology that already exists.

History is full of examples of companies who did not pioneer their core

offering, but came to dominate it anyway. Think of the way that Apple

has come to redefine and dominate the market for mobile devices—a

category pioneered by Motorola. Boeing did not pioneer modern jet

travel, nor Google the Internet search engine. Yet both companies are

now industry leaders.

In Seth's post he says:

No need to fool yourself into holding back just because your

innovation or product doesn't contain a flavor that's never been

tasted before or an experience previously unimagined.

I believe this, but what about the other end of the spectrum? For

instance:

This is a terrible quality video, but the only

one I could find.

We make fun of the five thousandth To-Do app, or the social network for

X. NOOOO, not another project management tool. Anybody want to build

another CMS?

There's been tons of silly ideas (and as developers we've built them)

yet occasionally something new will surface that competes with the

industry leader and even surpasses it. What made Slack different from

Hip Chat? What made Gmail different than yahoo mail? I'm not that

knowledgeable about all the different startup successes and failures, so

you fill in a few blanks of the ones you know.

My question is, when are competiting products valid? When are they seen

as another lousy idea?

In business school, I frequently thought of the old business tycoons who

were in the beginning of their industry's heyday: Henry Ford (autos),

J.P. Morgan (banking), Cornelius Vanderbilt (shipping and railroad

tycoon), John D. Rockefeller (oil). I'd think, if I'd been born then,

business would've been easy. In hindsight, it all seems so obvious:

trains, growth, ships, oil, investment, factories, etc. etc.

For the last couple of years, I've been wanting to create a business (in

addition to my consulting) around a SaaS (software as a service)

product. Since probably 2005, SaaS businesses have grown rapidly. Now it

seems there's an app for everything and anything. I've become to think

that the SaaS market is saturated and opportunity is few and far

between. If this is true, this also affects my consulting business

because if the opportunity isn't there, then less and less

entrepreneurs will need my consulting to help build software.

So like many entrepreneurs, I began to feel pessimistic and downcast about

the future. But like most entrepreneurs, this was a brief spell.

I recently read an article that bolstered my confidence: "You are not

late". The author talks about a similar thought process as I

mentioned above, but within the technology boom. "Oh, if we'd just been

around at the beginning of the dot com boom...things would have been so

easy." Then he says that:

If we could climb into a time machine and journey 30 years into the

future, and from that vantage look back to today, we'd realize that

most of the greatest products running the lives of citizens in 2044

were not invented until after 2014.

I believe that. Heck, 10 years from now, we probably won't be using the

majority same tools, services, and technologies we're using today. Major

platforms like the web and email may still be around, but they'll

probably look vastly different. For example, 5 years ago, the majority

of all email was hosted on an exchange server, or an in-house pop mail

server. Now, the majority of people access their email in the cloud

through different devices and clients.

Because here is the other thing the people in 2044 will tell you:

Can you imagine how awesome it would have been to be an entrepreneur

in 2014? It was a wide-open frontier!

The one thing that is constant is change and people have been innovating

since the beginning of time. There's opportunity in the future. You have

to be willing to learn, change and visualize if you want to take

part!

So now the hard part...what's next? What's the next big shift in

technology? What will are you working and investing your time?

This morning I read a Quora question posted by a student who wanted

to learn Ruby on Rails, but wanted to know how easy or difficult it was

to get a rails job.

I really like the response from a developer at Spotify. He said that

right now, it's easy to get a rails job and it pays competitively with

other like developer positions.

However, he said you cannot hang your hat on any one technology. If you

want to be a great developer, you have to be prepared to learn

constantly.

Constant learning is only behaviour that is guaranteed to get you

hired at the best companies and to give you job security as a

programmer. This is common to all great and well-paid developers -

develop a hunger for learning. Learn because it fascinates you, not

because it will land you a job. Ironically, it is this attitude that

WILL land you the best jobs, and give you security long-term.

I agree. When I started my company in 2008, I was constantly astonished

by the degree with which each project differed. I always told my wife,

if I could just get one project that was like the last we could really

make a profit. The truth is, even if you do get two projects that are

similar, if they are more than 6 months apart, some technology is going

to have a different "better" way of implementation.

Now, that's not to say that experience doesn't account for anything. It

does in a big way. When you have to update a gem or software

version, the more experienced you are, the more quickly you'll adapt, but

you'll never stop learning. If you do stop learning, you're likely

going to get left behind.

For the last few years, I've been extremely focused on rails and have

been reluctant to "play" with any other technologies or frameworks. I

didn't want anything to distract me from my focus on rails. Recently

however, as I've become a more mature rails developer and feel more

comfortable in that role, I've been wanting to branch out and learn some

new technologies. A few on at the top of my list are:

Yesterday I was out on a bike ride with my friend Matt Smith and he

told me he'd been challenged to write a blog post every business day for

the next 30 days. He didn't call me out like the Ice bucket challenge,

but he asked if I wanted to do it too. So I accepted.

At the beginning of this year I decided I really wanted to write more.

I'd read about numerous people like Nathan Berry writing 1000 words

daily or John Saddingon's obsession with blogging and decided I wanted

it to be a part of what I do. So I thought I'd take some time and figure

out why should I write?

Why Write?

1. To get better at it

I've never been great at writing. I've always been better at Math than

Reading/Writing (my math score nearly doubled my English sore on my

SAT's). I realise I don't have a natural ability to write, but I believe

it is something you can vastly improve on if you practice at it. Writing

and communication is critical in any career, but I believe as much or more

so than anywhere it's critical in software development.

2. To Learn

Whenever I write something I'm able to turn a lot of incomplete ideas

and thoughts into something meaningful and organized. If it's a

technical post where I'm explaining something I've built or designed,

then I learn even more than what I did when I first built it.

3. To Teach

It's also an opportunity to teach. I met Dr. Maya Angelou once and had

dinner with her in her apartment. One of my favorite quotes from her is

When you get, give. When you learn teach. I've learned so much

from others sharing what they know. I've literally gained a 2nd education

from the internet. I'm hoping to just pass a little on!

4. To inspire creativity

To write is a creative process and I believe it just breeds more

creativity. I'm the most creative when I'm writing often. I'm more

creative as a developer, designer, marketer...just all around.

5. To be more open

I hope that by being open, honest, communicative, and sharing more about

my life that I'll meet more people, build better relationships, and

enable clients to be more comfortable because they already know a

little about who I am and how I think, how I operate, and what to

expect.

6. Opportunity

Hopefully my writing will bring an audience and an audience will bring

opportunities. Whether through client work or partnership opportunities

or my next business partner, writing can bring opportunity in the door.

Summary

This isn't meant to be an exhaustive list, but the top reasons on my

mind right now.

I've been running a small business now for 18

years and I think I've finally settled on a simple way I like to answer

the key question...are we making money and if so how much?

My business is incorporated, so I get paid as an employee and the

business has a separate set of financials. I've always found it

difficult to answer my own question of "how'd we do last month?" It kinda

gets confusing because money flows in all different ways: regular

paychecks, dividend withdrawals, profit sharing plans (retirement /

investments aka my 401(k)) and other business perks / assets

(healthcare, company car, etc, etc.). Sometimes the business checking

will be way up, but the next month it'll be way down...but it's not

necessarily down because of business expenses, maybe it was time for a

scheduled investment withdrawal, or we made a transfer to a savings

account, or...

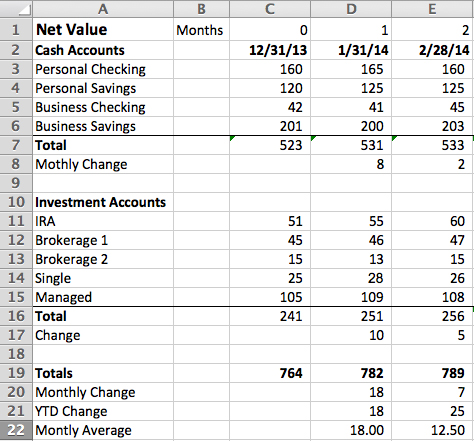

So what I started doing is on the first of every month is I compile a

list of all my "current cash and investment accounts." It's just a

simple excel sheet that looks something like this:

It adds all of your cash accounts like checking and savings, personal as

well as business. Then it adds all of your investment accounts. I

always enter these numbers at the exact same time every month. I do mine

early in the morning on the 1st of the month so I'm getting my cash

account and investment numbers for the close of business at month end.

Now this might look pretty simple, but in the myriad of financial

statements you can generate, this is a straight forward indicator of

whether or not you're building wealth / value.

What about financial statements?

I have an accountant that gives me all sorts of valuable statements like

an income statement, balance sheet, statement of cash flows, etc. Those

are important, but one main problem is that my business and I are really

one in the same. If I make a personal withdrawal from the business, my

cash flow statement will show a deduction, but my personal account will

show the addition. I want to know what's going on overall. It's a good

idea to keep your business and personal accounting separate, but if you

own a small business, you want some way to track an overall value. Not

that it should, but as far as I'm aware, there's not any accounting

software that will give you a snapshot across multiple companies /

personal accounts.

Not representative of productivity

One thing to note is that this is not an indicator of productivity on

the previous month. You might have a killer month, but not get paid for

it until the following month. It's really about keeping track of added

(or hopefully not reduced value) over the course of time.

Two indicators

I like seeing the monthly change in value, but the main two I look at

are the YTD Change and the Monthly Average.

The YTD Change lets me know overall if I'm adding value to my net worth.

Over the last 12 months, did I build value, maintain, or loose value?

The Monthly average let's me know on average how much extra cash (if

any) I have available each month. It helps answer questions like: can we

afford a new car payment, or can we increase our monthly retirement

contribution or can we increase giving to our church? As a small

business owner, your income is far from fixed, so answering those types

of questions are difficult. This indicator gives you a little insight.

Summary

I hope that might help someone out there. This is definitely no

substitute for real accounting software and/or an accountant, but it's a

nice snapshot of where you're at and how much you've grown.

Here's the excel file if you want to download it and customize it for

your own use. Let me know if you add anything to it or have other

methods for your financial analysis.